What is Supply?

Supply is an economic principle can be defined as the quantity of a product that a seller is willing to offer in the market at a particular price within specific time.

The supply of a product is influenced by various determinants, such as price, cost of production, government policies, and technology. It is governed by the law of supply, which states a direct relationship between the supply and price of a product, while other factors remaining the same.

Table of Content

A market is a place where buyers and sellers are engaged in exchanging products at certain prices.

In a market, the two forces demand and supply play a major role in influencing the decisions of consumers and producers.

The behaviour of buyers is understood with the help of the concept of demand. On the other hand, the behaviour of sellers is analysed using the concept of supply.

Also Read: Laws of Economics

Concept of Supply

What is Supply Concept? In economics, supply refers to the quantity of a product available in the market for sale at a specified price and time.

In other words, supply can be defined as the willingness of a seller to sell the specified quantity of a product within a particular price and time period. Here, it should be noted that demand is the willingness of a buyer, while supply is the willingness of a supplier.

Also Read: What is Business Economics?

Meaning of Supply

What is Supply Meaning? Supply has three important aspects, which are as follows:

- Supply is always referred in terms of price

The price at which quantities are supplied differs from one location to the other.

For example, fast moving consumer goods (FMCG) are usually supplied at different prices in different prices. - Supply is referred in terms of time

This means that supply is the amount that suppliers are willing to offer during a specific period of time (per day, per week, per month, bi-annually, etc.) - Supply considers the stock and market price of the product

Both stock and market price of a product affect its supply to a greater extent. If the market price of a product is more than its cost price, the seller would increase the supply of the product in the market. However, a decrease in the market price as compared to the cost price would reduce the supply of product in the market.

Also Read: Law of Supply

Supply Definition

What is Supply Definition? Economist has given different supply definition but the essence is same.

Also Read: What is Supply Schedule?

Supply Example

What is Supply? Let us understand the concept of supply with an example.

For example, a seller offers a commodity at 100 per piece in the market. In this case, only commodity and price are specified; thus, it cannot be considered as supply.

However, there is another seller who offers the same commodity at 110 per piece in the market for the next six months from now on. In this case, commodity, price, and time are specified, thus it is supply.

Also Read: What is Supply Curve?

Classification of supply

What is Supply Classification? Supply can be classified into two categories, which are individual supply and market supply.

- Individual supply is the quantity of goods a single producer is willing to supply at a particular price and time in the market. In economics, a single producer is known as a firm.

- Market supply is the quantity of goods supplied by all firms in the market during a specific time period and at a particular price. Market supply is also known as industry supply as firms collectively constitute an industry.

Also Read: Movement and Shift along Supply Curve

Types of Supply

- Market Supply

- Short-term Supply

- Long-term Supply

- Joint Supply

Also Read: What is Demand Curve?

Determinants of Supply

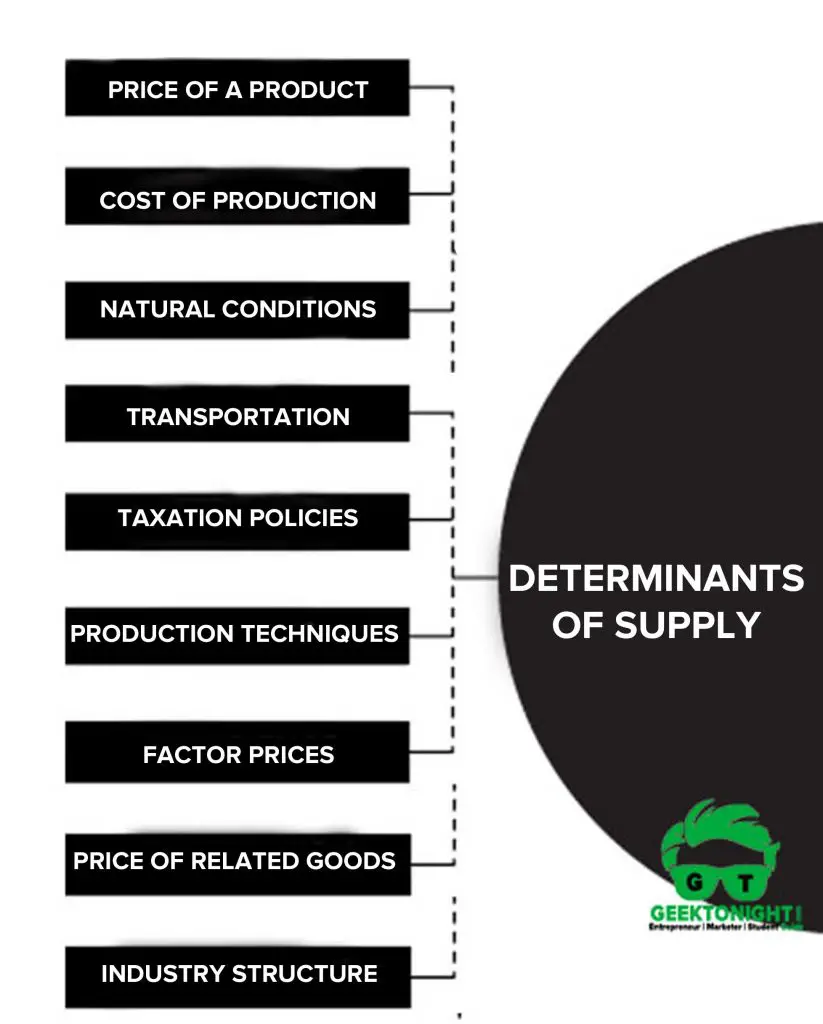

9 Determinants of supply are:

- Price of a product

- Cost of production

- Natural conditions

- Transportation conditions

- Taxation policies

- Production techniques

- Factor prices and their availability

- Price of related goods

- Industry structure

Price of a product

The major determinants of the supply of a product is its price. An increase in the price of a product increases its supply and vice versa while other factors remain the same.

Cost of production

It is the cost incurred on the manufacturing of goods that are to be offered to consumers. Cost of production and supply are inversely proportional to each other.

Natural conditions

The supply of certain products is directly influenced by climatic conditions. For instance, the supply of agricultural products increases when the monsoon comes well on time.

Transportation conditions

Better transport facilities result in an increase in the supply of goods. Transport is always a constraint to the supply of goods. This is because goods are not available on time due to poor transport facilities.

Taxation policies

Government’s tax policies also act as a regulating force in supply. If the rates of taxes levied on goods are high, the supply will decrease. This is because high tax rates increase overall productions costs, which will make it difficult for suppliers to offer products in the market.

Production techniques

The supply of goods also depends on the type of techniques used for production. Obsolete techniques result in low production, which further decreases the supply of goods.

Factor prices and their availability

The production of goods is dependent on the factors of production, such as raw material, machines and equipment, and labour.

The prices of substitutes and complementary goods also influence the supply of a product to a large extent.

Industry structure

The supply of goods is also dependent on the structure of the industry in which a firm is operating. If there is monopoly in the industry, the manufacturer may restrict the supply of his/her goods with an aim to raise the prices of goods and increase profits.

Also Read: Law of Supply

Supply Function

Supply function is the mathematical expression of law of supply. In other words, supply function quantifies the relationship between quantity supplied and price of a product, while keeping the other factors at constant.

The law of supply expresses the nature of the relationship between quantity supplied and price of a product, while the supply function measures that relationship.

The supply function can be expressed as:

Qs = f (Pa, Pb, Pc, T, Tp)

Where,

Qs = Supply

Pa = Price of the good supplied

Pb = Price of other goods

Pc = Price of factor input

T = Technology

Tp = Time Period

According to the supply function, the quantity supplied of a good (Qs) varies

with the price of that good (Pa), the price of other goods (Pb), the price

of factor input (Pc), the technology used for production (T), and time period

(Tp)

Business Economics Tutorial

(Click on Topic to Read)

Go On, Share article with Friends

Did we miss something in Business Economics Tutorial? Come on! Tell us what you think about our article on What is Supply | Business Economics in the comments section.

Business Economics Tutorial

(Click on Topic to Read)

I wish to be always be updated When New information comes