The advertising budget of a business is typically a subset of the larger sales budget and, within that, the marketing budget. Advertising is a part of the sales and marketing effort. Money spent on advertising can also be seen as an investment in building up the business.

Table of Content

In order to keep the advertising budget in line with promotional and marketing goals, a business owner should start by answering several important questions:

- Who is the target consumer?

- Who is interested in purchasing the product or service?

- What are the specific demographics of this consumer (age, employment, sex, attitudes, etc.)?

Often it is useful to compose a consumer profile to give the abstract idea of a “target consumer” a face and a personality that can then be used to shape the advertising message.

- What media type will be most useful in reaching the target consumer?

- What is required to get the target consumer to purchase the product?

- Does the product lend itself to rational or emotional appeals?

- Which appeals are most likely to persuade the target consumer?

- What is the relationship between advertising expenditures and

- What is the impact of advertising campaigns on product or service purchases?

Answering these questions will help to define the market conditions that are anticipated and identify specific goals the company wishes to reach with an advertising campaign. Once this analysis of the market situation is complete, a business must decide how best to budget for the task and how best to allocate budgeted funds.

The budget is an estimation of future advertising expenditure that will be used to implement managerial decisions, to maintain or improve profit result.

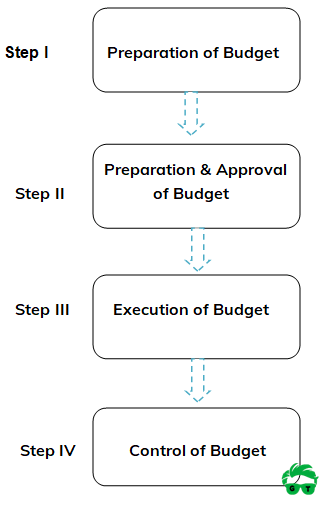

Procedures of Budgeting

The advertising budgeting procedure involved following stages;

- Preparation of Budget: The advertising budget generally prepared by the advertising manager in consultation with marketing manager. The advertising budget mainly made on the basis of inputs such as; type of product, target market, demographic composition, advertising copy, and media; provided by the marketing research people.

- Presentation and Approval of Budget: Once the advertising budget prepared by the advertising managers, it is presented in front of the top management for the approval.

- Execution of the Budget: After approval, the approval process, the advertising manager execute the overall budget. At the time of execution, the budget allocation are to be considered for various activities.

- Control of Budget: Once the advertising department of an organization execute the budget, the result come out. So in this stage of advertising budget process, the management ensures the correct use of advertising budget by evaluating the overall effectiveness of advertising programme.

Allocation of Advertising Budget

Following main aspects of a company which are considered by the management at the time of allocating the advertising budget on different activities.

- Marketing Mix of the Company: Product, Price, Place, & Promotion

- The sales forecast

- Affordability (How much funds organization can invest)

- The product life cycle

- Type of the product

- Quality of the campaign: If the advertising campaign is of high quality needed small budget

- Level of competition

- The budgeting cycle: (time period of budget), if budget made for six month, lesser money will be required then the budget for one year

- Contingency Planning: There are many external uncontrollable restraints that must be taken into consideration while planning the budget

Advertising Budget Methods

Following are the main approaches used by the companies while setting the limit of advertising expenditure.

- Top-Down Approach or Affordable Method

- Bottom-Up Approach or Build-Up Approach

Advertising Budget Methods are:

- Percentage of Sales Method

- Arbitrary Allocation Method

- Competitive Parity Method

- Return on Investment (ROI) Method

- Objective and task method

- Payout planning method

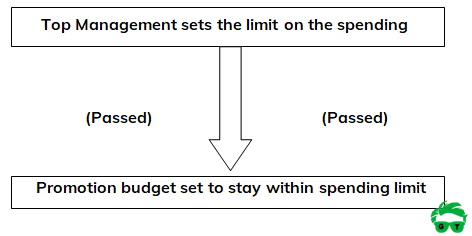

Top-Down Approach or Affordable Method

When the budget amount or expenditure limit for advertising is established by the top management of the organization and then passed down to the various department called top-down approach.

The top-down approach of budget setting includes following methods:

- Percentage of Sales Method

- Arbitrary Allocation Method

- Competitive Parity Method

- Return on Investment (ROI) Method

Percentage of Sales Method: This method is one of the most widely used method for setting the appropriation. “Percentage of sales method is based on the previous year’s sales, on estimated sales of coming year or on some combination of these two”

This method include following two:

- Straight percentage of sales: In this method sales are project for the coming year based on the marketing manager’s estimation.

2020 – Total Rs Sales – Rs 10,000,00 Straight percentage of sales at 10% – Rs 1,00,000

2021 – Advertising Budget – Rs 1,00,000 - Percentage of unit cost. 2020 – Cost per bottle to manufacture – Rs 4.00 Unit cost allocated to advertisement – Rs 1.00

2020 – Forecasted Sales Rs 10,000 units 2015-Advertising Budget (10,000×1)-Rs 10,000

Arbitrary Allocation Method: In this method, the budget is determined by the manager solely (alone) on the basis of his/her judgment, or without any rationality or rule.

Competitive Parity Method: While keeping one’s own objectives in mind, it is often useful for a business to compare its advertising spending with that of its competitors. The theory here is that if a business is aware of how much its competitors are spending to advertise their products and services, the business may wish to budget a similar amount on its own advertising by way of staying competitive.

Doing as one’s competitor does is not, of course, always the wisest course. And matching another’s advertising budget dollar for a dollar does not necessarily buy one the same marketing outcome. Much depends on how that money is spent. However, gauging one’s advertising budget on other participants’ in the same market is a reasonable starting point.

Return on Investment (ROI) Method: This method, also referred to as ‘rate on investment’ or ‘incremental method’, considers advertising and promotion as investments, like plant and equipment.

Therefore, investment in the budgetary appropriation i.e. expenditure on advertising and promotion is expected to bring certain returns. This method measures the return in terms of increased sales on spending advertisement appropriation in comparison to the sales on not spending anything.

Bottom-Up Approach or Build-Up Approach

In this strategy the organization first determine all activities which are necessary for performing overall communication task and allocate funds on them, then the top management of the organization approve the limit as per needed task.

The bottom-up approach includes following methods:

Objective and task method: The objective and task method includes the following three steps.

- Defining the communication objectives to be accomplished.

- Determining the specific strategies and task needed to attain them.

- Estimating the costs associated with performance of these strategies and tasks.

Payout planning method: The method is widely used for making advertising budget for the new product. A payout plan is developed to determine how much to spend.” The basic idea behind payout planning method is to project the revenues the product will generate over two or three years, as well as the cost it will incur.”

This method is based on the expected rate of return. This method is helpful for determining how much advertising expenditures will be necessary when the return might be expected.

Marketing Management

(Click on Topic to Read)

- What Is Market Segmentation?

- What Is Marketing Mix?

- Marketing Concept

- Marketing Management Process

- What Is Marketing Environment?

- What Is Consumer Behaviour?

- Business Buyer Behaviour

- Demand Forecasting

- 7 Stages Of New Product Development

- Methods Of Pricing

- What Is Public Relations?

- What Is Marketing Management?

- What Is Sales Promotion?

- Types Of Sales Promotion

- Techniques Of Sales Promotion

- What Is Personal Selling?

- What Is Advertising?

- Market Entry Strategy

- What Is Marketing Planning?

- Segmentation Targeting And Positioning

- Brand Building Process

- Kotler Five Product Level Model

- Classification Of Products

- Types Of Logistics

- What Is Consumer Research?

- What Is DAGMAR?

- Consumer Behaviour Models

- What Is Green Marketing?

- What Is Electronic Commerce?

- Agricultural Cooperative Marketing

- What Is Marketing Control?

- What Is Marketing Communication?

- What Is Pricing?

- Models Of Communication

Sales Management

- What is Sales Management?

- Objectives of Sales Management

- Responsibilities and Skills of Sales Manager

- Theories of Personal Selling

- What is Sales Forecasting?

- Methods of Sales Forecasting

- Purpose of Sales Budgeting

- Methods of Sales Budgeting

- Types of Sales Budgeting

- Sales Budgeting Process

- What is Sales Quotas?

- What is Selling by Objectives (SBO)?

- What is Sales Organisation?

- Types of Sales Force Structure

- Recruiting and Selecting Sales Personnel

- Training and Development of Salesforce

- Compensating the Sales Force

- Time and Territory Management

- What Is Logistics?

- What Is Logistics System?

- Technologies in Logistics

- What Is Distribution Management?

- What Is Marketing Intermediaries?

- Conventional Distribution System

- Functions of Distribution Channels

- What is Channel Design?

- Types of Wholesalers and Retailers

- What is Vertical Marketing Systems?

Marketing Essentials

- What is Marketing?

- What is A BCG Matrix?

- 5 M'S Of Advertising

- What is Direct Marketing?

- Marketing Mix For Services

- What Market Intelligence System?

- What is Trade Union?

- What Is International Marketing?

- World Trade Organization (WTO)

- What is International Marketing Research?

- What is Exporting?

- What is Licensing?

- What is Franchising?

- What is Joint Venture?

- What is Turnkey Projects?

- What is Management Contracts?

- What is Foreign Direct Investment?

- Factors That Influence Entry Mode Choice In Foreign Markets

- What is Price Escalations?

- What is Transfer Pricing?

- Integrated Marketing Communication (IMC)

- What is Promotion Mix?

- Factors Affecting Promotion Mix

- Functions & Role Of Advertising

- What is Database Marketing?

- What is Advertising Budget?

- What is Advertising Agency?

- What is Market Intelligence?

- What is Industrial Marketing?

- What is Customer Value

Consumer Behaviour

- What is Consumer Behaviour?

- What Is Personality?

- What Is Perception?

- What Is Learning?

- What Is Attitude?

- What Is Motivation?

- Segmentation Targeting And Positioning

- What Is Consumer Research?

- Consumer Imagery

- Consumer Attitude Formation

- What Is Culture?

- Consumer Decision Making Process

- Consumer Behaviour Models

- Applications of Consumer Behaviour in Marketing

- Motivational Research

- Theoretical Approaches to Study of Consumer Behaviour

- Consumer Involvement

- Consumer Lifestyle

- Theories of Personality

- Outlet Selection

- Organizational Buying Behaviour

- Reference Groups

- Consumer Protection Act, 1986

- Diffusion of Innovation

- Opinion Leaders

Business Communication

- What is Business Communication?

- What is Communication?

- Types of Communication

- 7 C of Communication

- Barriers To Business Communication

- Oral Communication

- Types Of Non Verbal Communication

- What is Written Communication?

- What are Soft Skills?

- Interpersonal vs Intrapersonal communication

- Barriers to Communication

- Importance of Communication Skills

- Listening in Communication

- Causes of Miscommunication

- What is Johari Window?

- What is Presentation?

- Communication Styles

- Channels of Communication

- Hofstede’s Dimensions of Cultural Differences and Benett’s Stages of Intercultural Sensitivity

- Organisational Communication

- Horizontal Communication

- Grapevine Communication

- Downward Communication

- Verbal Communication Skills

- Upward Communication

- Flow of Communication

- What is Emotional Intelligence?

- What is Public Speaking?

- Upward vs Downward Communication

- Internal vs External Communication

- What is Group Discussion?

- What is Interview?

- What is Negotiation?

- What is Digital Communication?

- What is Letter Writing?

- Resume and Covering Letter

- What is Report Writing?

- What is Business Meeting?

- What is Public Relations?

Business Law

- What is Business Law?

- Indian Contract Act 1872

- Essential Elements of a Valid Contract

- Types of Contract

- What is Discharge of Contract?

- Performance of Contract

- Sales of Goods Act 1930

- Goods & Price: Contract of Sale

- Conditions and Warranties

- Doctrine of Caveat Emptor

- Transfer of Property

- Rights of Unpaid Seller

- Negotiable Instruments Act 1881

- Types of Negotiable Instruments

- Types of Endorsement

- What is Promissory Note?

- What is Cheque?

- What is Crossing of Cheque?

- What is Bill of Exchange?

- What is Offer?

- Limited Liability Partnership Act 2008

- Memorandum of Association

- Articles of Association

- What is Director?

- Trade Unions Act, 1926

- Industrial Disputes Act 1947

- Employee State Insurance Act 1948

- Payment of Wages Act 1936

- Payment of Bonus Act 1965

- Labour Law in India

Brand Management